Vladislav Inozemtsev: A collapse is not imminent

The Iran ceasefire has sent oil prices sliding, and with them, Russia’s biggest wartime revenue stream.

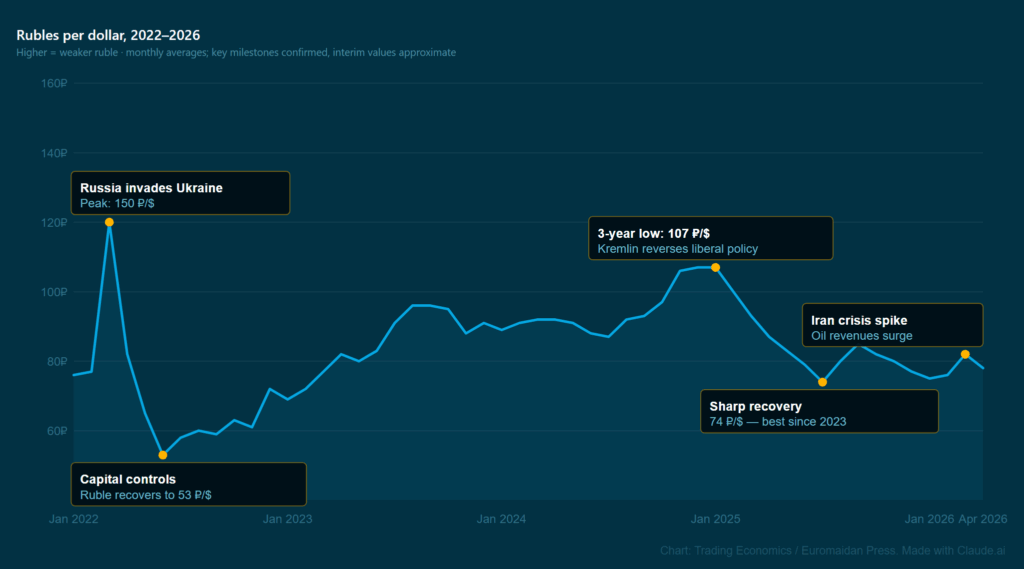

Vladislav Inozemtsev, Ph.D. in economics, is a co-founder and senior fellow at the Center for Analysis and Strategies. Russia’s seaborne oil exports earned $2.02 billion a week in the four weeks to 5 April 2026—the highest since June 2022—before a two-week fictitious ceasefire in the Iran war pushed prices marginally lower.

Euromaidan Press spoke with him about what the oil surge means for Russia’s war budget, why Ukrainian strikes on export ports matter more than hits on refineries, and why the economists predicting Russia’s imminent collapse are just in it for the popularity.

Peeter Helme: How do you assess the situation for Russia’s economy in light of the Iran ceasefire and the drop in oil prices?

Vladislav Inozemtsev: Trump’s policies are very unpredictable, and I don’t think we will see a steep decline in prices—and even less probable is their return to pre-crisis levels. Global reserves have been partially depleted during this period of uncertainty, and everyone has now witnessed how fragile the oil market is and how significant supply cuts can be. To my mind, Brent prices will not recede to around $70–75 till the end of the year.

I have doubts that the American administration will restore the previous sanctions regime.

There is also the question of sanctions. When President Trump issued a waiver to India and other countries allowing them to buy Russian oil, it was the first precedent of easing sanctions since 2014—and a very important one.

It seems that these waivers are already extended for the April-May period, and I have doubts that the American administration will restore the previous sanctions regime in general, because its allies can now easily argue: you have seen how problematic supply disruptions can be. There will be quite strong pressure on Trump—from India, from South Korea, and from other countries—not to restore them.

Russia is still a significant winner here, and its financial situation will improve greatly compared to what was assumed at the end of February.

Peeter: How big an impact are Ukrainian strikes on Russian oil ports and refineries having on Russia’s ability to collect revenues from oil sales?

Inozemtsev: It is an important point, but it shouldn’t be overestimated.

When Ukraine started attacking Russian oil facilities last summer, a lot of processing enterprises were struck. I had commented at that time that strikes against oil refineries are much more effective than strikes against military enterprises.

Knock out the export facilities, and the budget faces real problems.

If you target a refinery, you cause massive destruction—fires that can last for days or even weeks. A military enterprise you cannot destroy entirely: you hit one subdivision, and it is restored by the end of the week.

But strikes on export facilities are even more effective than strikes on refineries. If you hit a refinery, the Russians simply export crude instead of processed petroleum, and crude brings the state approximately the same amount of money either way. Knock out the export facilities, and the budget faces real problems. The strategy has improved, and the effectiveness has improved accordingly.

With prices having risen two and a half times, Russia still earns more revenue than before.

Some numbers: in March, the price of Russian oil rose from around $42–45 per barrel to around $100. Russia exports roughly 6.5–7 million barrels a day, with about one-third going east by pipeline to China or through Pacific ports, around 40% through Baltic Sea ports, and around 25% through Novorossiysk and other Black Sea ports.

If you attack Novorossiysk, Primorsk, or Ust-Luga and knock out 40% of capacity—as some Western analysts have estimated—you disable roughly 25% of Russian exports. That is a huge amount. But with prices having risen two and a half times, Russia still earns more revenue than before.

I would advise the Ukrainian authorities not to respond to the calls from Europe to stop the strikes.

Stopping all deliveries from the Baltic and Black Sea would be a decisive blow—but it is practically impossible, because they repair the facilities—apparently at remarkable speed. Still, every successful strike may deprive Russian oil companies of around $100 million worth of oil that has been kept in reservoirs, and any urgent repairs and restorations take a great deal of money, probably millions of dollars.

So, I would advise the Ukrainian authorities not to respond to the calls from Europe to stop the strikes because oil prices are too high. The war is underway. You are protecting your country, defending yourself and your loved ones, and therefore have no alternative but to damage your enemy as much as possible.

This is the most effective thing you can do economically—but I don’t think it will either ruin the Russian budget or force Putin to rethink his strategy.

Peeter: Can we say that, because of this rapid rise in oil prices, the Russian budget—which was in trouble—has been saved for this year?

Inozemtsev: In December, when most experts were predicting catastrophic trouble for the Russian budget, my position was that the Finance Ministry would most probably devalue the ruble and thereby increase ruble-denominated revenues even if the oil price stayed around $40 per barrel.

Current spot prices touched $150 per barrel last week.

Instead, prices went up significantly in March and remain elevated in April. Since the commodity exchanges indicate futures pricing, one should be aware that deals that are being concluded now reflect the prices for the rest of April, all of May, and early June. Current spot prices touched $150 per barrel last week. Most Russian oil will almost certainly be sold at around $100 per barrel in both April and May.

If prices fall in the coming weeks—which remains unlikely—contract prices will depreciate starting from late May. But Russia would still have at least three months of very comfortable conditions, bringing the budget closer to the projections adopted by the State Duma in October 2025.

If the Kremlin feels that budget pressure is easing, it will simply increase military expenditures.

With quite a high probability, Russia will execute the 2026 budget more or less as adopted last year. There is no immediate danger of a 10 trillion ruble ($128 billion) deficit—as some clickbait economists assumed in January—but equally, there is no chance of any surplus—at least because, in case it happens, the Russian Finance ministry would consider these funds “additional revenues” and use them for various programs during the same financial year.

So, if the Kremlin feels budget pressure easing, it will simply increase military expenditures. The real economy will not profit much from recent developments.

Peeter: Last year, we saw nervousness from the Russian Central Bank—repeatedly raising and lowering key interest rates. Does this show friction between Russia’s political elite and the Central Bank, with one pushing financial orthodoxy and the other imposing political priorities?

Inozemtsev: The problem of the Central Bank, to my mind, is its leadership’s obsession with Western economic doctrine. It raised key rates starting in 2024 to combat inflation, as if Russia resembled the United States, with its competitive economy and monetary factors dominating price dynamics.

Together, they strangled economic growth in 2025.

In Russia, inflation is not so much monetary as the result of coordinated price hikes by the government, which allows state monopolies to raise tariffs, which raise taxes, which raise everything else. Interest rates alone cannot fix that.

The government was actually in full solidarity with the Central Bank, because both fear public discontent over rising prices—any poll confirms that prices are the primary concern of Russian consumers. The result: both institutions became simultaneously unconcerned with growth, entrepreneurial sentiment, and the business climate. Together, they strangled economic growth in 2025. Entirely self-inflicted.

Peeter: Following Russian provincial newspapers, one gets the impression that what you’ve been describing is producing real discontent on the ground, as small business owners and ordinary people alike complain about rising prices and higher taxes. Would you agree with that reading?

Inozemtsev: Absolutely. The policy went wrong at least from 2024.

The major concern in a situation like Russia’s should be economic growth—the business climate, jobs, tax revenues. And in 2022, when the government reacted to the war and the first waves of sanctions, that is what happened.

Taxes were left untouched from 2022 through 2024.

I would say 2022 saw the most liberal economic policy in Russia since 2001-2002: they liberalized imports through parallel import schemes, introduced credit holidays and a bankruptcy moratorium, eased banking regulations allowing banks to distribute far more loans.

The volume of subsidized mortgages hit all-time highs. Taxes were left untouched from 2022 through 2024. This liberal economic course produced real results—hefty growth in 2023 and 2024.

For whatever reason I cannot explain—the magnitude of Putin’s idiotism is immeasurable—he then believed it was time to do the opposite. Increase taxes, increase regulation on every possible sphere, and deprive small businesses and the self-employed of their benefits. Apparently to solve his financial problems. Why? Don’t ask me.

Before the war, coal accounted for around 30% of all ton-kilometers of rail freight—a heavily subsidized sector now in terrible condition.

And yet all the Russian opposition economists who want to be popular on YouTube talk about a full collapse coming tomorrow—every day. You see a headline saying the Russian economy is collapsing, but the article says shipments on Russian railways decreased by 8% last year.

For anyone a little familiar with the Russian transportation system, that figure simply means the railways reduced coal shipments. Before the war, coal accounted for around 30% of all ton-kilometers of rail freight—a heavily subsidized sector now in terrible condition, for obvious reasons.

The same is true of the building materials industry. These two categories easily explain the drop in transportation volumes. Some industries are in genuine crisis—but that does not affect services, agriculture, the oil industry, or many other sectors.

Zero growth, minus 1%, minus 2%, regional problems, deep trouble in specific industries—that is painful, but it happens.

A serious crisis would look like this: a 6% or more contraction in GDP, a 20–30% ruble devaluation, and a 15% or more decrease in real disposable incomes. If that happens, the economy will be on the verge of something deserving the word “collapse.”

Zero growth, minus 1%, minus 2%, regional problems, deep trouble in specific industries—that is painful, but it happens, and anyone should be rather surprised if it did not happen after four years of war.

The Russian economy is more or less sustainable. It produces record tax revenues for the government. If it does collapse eventually, it will be entirely because of Kremlin policies—Western sanctions account for perhaps 3% of that risk. A collapse is not imminent.

Peeter: You mentioned rising prices as a key public concern. Why does economic discontent not translate into political pressure on the Kremlin?

Inozemtsev: To be motivated by economic issues, people need to feel that those issues demonstrate the system of governance is defunct. In Soviet times, everyone received their salary, then went to the shops and found empty shelves. That was a powerful demonstration: you work, you earn, you cannot buy. The system doesn’t function.

If you don’t have money while many others do, and everything is on offer, you blame yourself.

Now the situation is completely different. The shops are full. You can buy a ticket and vacation anywhere—if you have money. But many people do not have money. And this produces a completely different attitude. If you don’t have money while many others do, and everything is on offer, you blame yourself. You haven’t found your place in an affluent society. It is your personal failure—not the system’s.

Individual discontent will not turn into a mass protest for this reason.

Consider what happened in February 2015. Navalny received permission to hold a street rally in Moscow—a march against the economic crisis. He had an extensive network of supporters and ran a campaign to estimate turnout.

Two days before the event, 3,500 people from this multi-million-person city had signed up. That night, Boris Nemtsov was killed in the center of Moscow. The march was rededicated to his memory, and 70,000 people showed up.

Political issues can ignite people’s will.

That is the difference between economic grievances and political ones. Political issues can ignite people’s will. Economic issues, on their own, will not.

Don’t expect Russians to go to the barricades over economic hardship.

Peeter: What is the most important thing Western policymakers and audiences are missing about Russia’s war economy?

Inozemtsev: The most encouraging developments in recent months have been Ukrainian military successes on the front line. Everyone in Russia is aware of the situation there, regardless of what the Ministry of Defense says about record numbers of contract soldiers.

The more attention you give to Russian economic problems and the less you concentrate on military capability, the worse it will be.

Ukrainian drone attacks in March were almost twice as intense as Russian ones. Ukraine is making real progress, and it is encouraging that it came in 2026—though it should have come sooner.

From the very start of the war, I have said—and I repeat—that wars cannot be won by sanctions. They must be won on the ground, maybe by drones, but by military means. The more attention you give to Russian economic problems and the less you concentrate on military capability, the worse it will be. That is the only way to bring Putin to a reality he actually understands.

Annihilating the Russian hordes is your main purpose.

The war will be won or lost on the front, not in EU headquarters, where the 20th package of sanctions is debated. Annihilating the Russian hordes is your main purpose. Targeting Russian export facilities is also fine because it has a direct military-economic impact.

But the idea that you can force Russia to the table by cutting off its gas revenues from 2027, or by pressing Singapore not to buy Russian oil—those are worthless diplomatic exercises. Don’t fool yourself that they will end the war.

They will not.